PF in India – EPF Rules, Benefits & Withdrawal Process Simplified 💼🇮🇳

Arre doston, ek baat bolo – har mahine jab salary credit ka SMS aata hai na, ekdum mast feel hota hai. Lekin jaise hi payslip kholte ho, ek line dil tod deti hai – “PF Deduction”. Aur hum youngsters (especially first job wale) aksar sochte hain – “Yaar ye bhi ek salary cut hi hai 😅.”

Lekin asli baat yeh hai ki PF in India (Provident Fund) ekdum strong savings + retirement tool hai. Agar tumhe iske rules, benefits aur withdrawal process acche se samajh aa jaye, toh yeh tumhare liye ek crore-plus retirement fund ban sakta hai.

Chalo aaj iss blog me hum mast friendly tareeke se samajhte hain – PF kya hai, kaise kaam karta hai, kya benefits deta hai aur kaise withdraw hota hai – with real-life examples.

PF in India kya hota hai? 🤔

Simple language me samjho – PF ek government-backed savings scheme hai jisme tum aur tumhara employer dono apni salary ka ek hissa jama karte ho.

- EPF (Employees’ Provident Fund): Ye private company ke salaried logon ke liye hota hai.

- Isse manage karta hai: EPFO (Employees’ Provident Fund Organisation).

👉 Matlab: Tum thoda paisa save karte ho, employer bhi utna hi add karta hai, aur saara paisa interest ke sath grow karta rehta hai till retirement.

PF in India kya hota hai? 🤔

Sab employees ko PF automatically nahi milta. Kuch rules hain:

- Agar company me 20 ya usse zyada employees hain toh PF mandatory hai.

- Agar tumhari basic salary + DA ≤ ₹15,000 hai toh PF compulsory hai.

- Agar salary > ₹15,000 hai, toh bhi tum PF join kar sakte ho, but with employer’s approval.

- Government + private dono employees ko PF mil sakta hai.

Example:

Rohit (24, IT job, basic ₹20,000) ka PF har mahine auto deduct hota hai. Lekin uski cousin Neha ek chhoti startup (8 employees) me kaam karti hai, usko PF nahi milta – jab tak company voluntarily opt-in na kare.

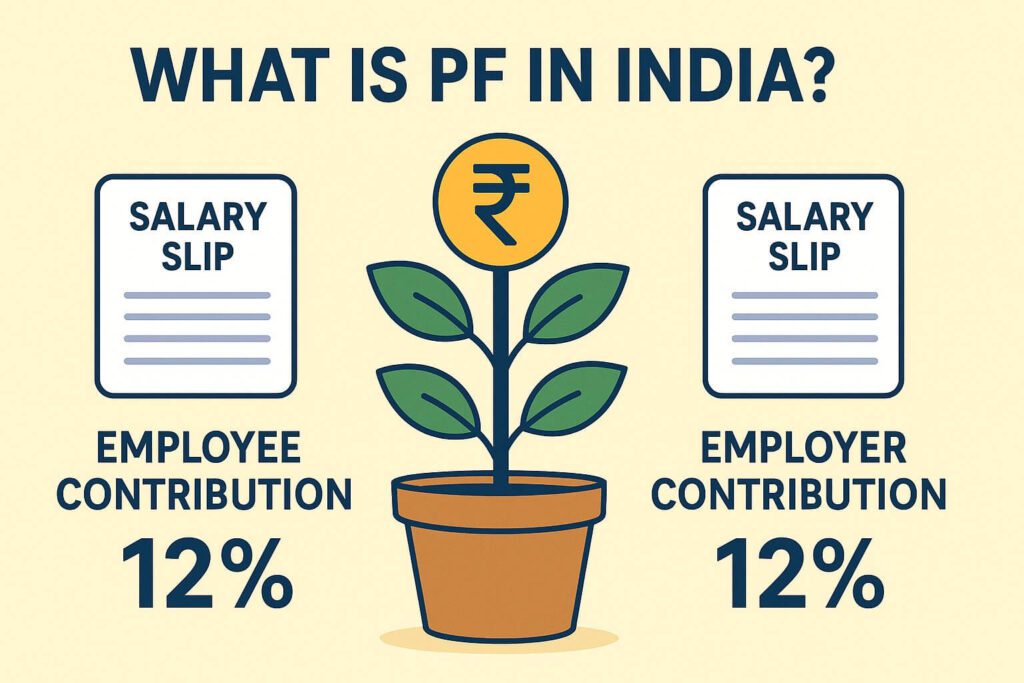

PF Contribution Kitna Hota Hai? 🧾

Har mahine tum aur tumhara employer dono 12% contribute karte hain tumhari basic salary + DA ka.

- Employee contribution: 12%

- Employer contribution: 12% (isme se kuch pension me jata hai)

Breakdown:

- Employer ka 8.33% → EPS (Employee Pension Scheme)

- Bacha hua 3.67% → EPF

Example:

Basic salary = ₹20,000

- Tumhare taraf se = ₹2,400

- Employer = ₹2,400

- ₹1,666 → EPS

- ₹734 → EPF

Total monthly = ₹4,800

1 saal me = ₹57,600 (plus ~8% interest)

Socho, ye chhota sa monthly deduction long-term me crore ban jata hai 🔥.

PF Interest Rate Kitna Hai? 📈

- FY 2024–25 ke liye PF interest = 8.25% p.a.

- Interest monthly calculate hota hai, but yearly credit hota hai.

Savings account (3–4% interest) se toh kaafi zyada fayda deta hai.

Benefits of PF in India 💡

1. Retirement ke liye ekdum safe fund

Job ke baad tumhare paas ek bada backup ready hota hai.

2. Employer Contribution = Free Money

Tumne ₹1 dala toh company bhi ₹1 daal rahi hai. Free investment growth! 😎

3. Tax Benefits

- Section 80C ke under ₹1.5 lakh tak deduction milta hai.

- Agar 5 saal baad withdraw karte ho toh pura tax-free.

4. Emergency me kaam aata hai

PF se loan/partial withdrawal kar sakte ho for:

- Home loan

- Marriage

- Education

- Medical emergency

5. Insurance Cover (EDLI)

PF members ko life insurance cover (upto ₹7 lakh) milta hai.

6. Pension bhi milega

EPS me jaane wala paisa retirement ke baad monthly pension ban jata hai.

“Aapko yeh concept pasand aa raha hai toh aapko yeh wala blog bhi kaafi useful lagega  [Salary Slip Explained in India – Full Breakdown of Basic, HRA, PF & Deductions

[Salary Slip Explained in India – Full Breakdown of Basic, HRA, PF & Deductions  ]”

]”

PF Withdrawal Rules India me 🏦

Yeh samajhna zaroori hai – PF kisi piggy bank jaisa nahi ki jab mann kiya withdraw kar liya. Kuch rules hote hain:

🔹 Complete Withdrawal

- Retirement (58 yrs) ke baad.

- Ya phir 2 months se unemployed ho.

🔹 Partial Withdrawal (special cases)

- Education / Marriage → 7 yrs ke baad 50%

- Medical emergency → anytime

- House buy/construct → 5 yrs ke baad 90% tak

🔹 Tax Rules

- 5 saal ke andar withdraw kiya toh taxable hai.

- 5 saal ke baad → pura tax-free.

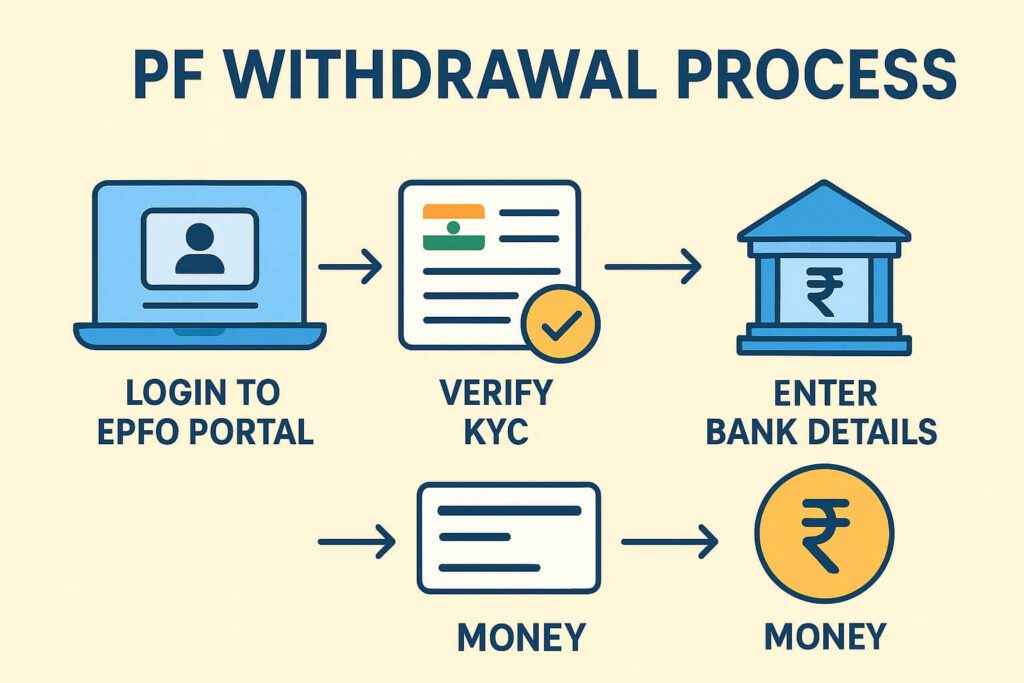

Online PF Withdrawal Process 💻

Ab toh process easy hai – bas UAN (Universal Account Number) activate hona chahiye.

Steps:

- EPFO UAN Portal par jao.

- UAN + password se login karo.

- Online Services → Claim (Form-31, 19, 10C & 10D).

- KYC verify karo.

- Withdrawal type select karo (Final Settlement / Pension / Partial).

- Bank details fill karo + docs upload (if required).

- Submit → within 10–15 din paisa account me.

Real-Life Example

Ritika (27, marketing job) ke paas ₹4.5 lakh PF tha. Higher studies ke liye usne partial withdrawal apply kiya. Lekin rule ke hisaab se 7 years complete hone chahiye the, aur usne 6 years hi kiya tha. Result? Pura paisa nahi mila. Usne PF loan liya.

👉 Lesson: PF withdrawal rules samajh lena zaroori hai before planning big expenses.

PF vs PPF – Confusion Clear Karo 🔄

- UAN activate nahi karna.

- Job change pe PF transfer nahi karna → multiple accounts mess.

- Jaldi PF withdraw kar lena (long-term compounding miss ho jata hai).

- EPS pension ignore karna.

- PF passbook check nahi karna (kabhi employer late contribution karta hai).

Common Mistakes Young Employees Karte Hain 🚫

- PF (EPF): Sirf salaried employees ke liye. Employer bhi contribute karta hai.

- PPF (Public Provident Fund): Har koi khol sakta hai – students, self-employed, housewives. Employer ka contribution nahi hota.

Smart move = Agar job kar rahe ho toh PF + PPF dono maintain karo for long-term wealth.

PF Balance Check Kaise Karein? 📲

- UMANG App (EPFO service).

- EPFO Portal (UAN login).

- SMS: “EPFOHO UAN ENG” to 7738299899.

- Missed call: 9966044425 from registered mobile.

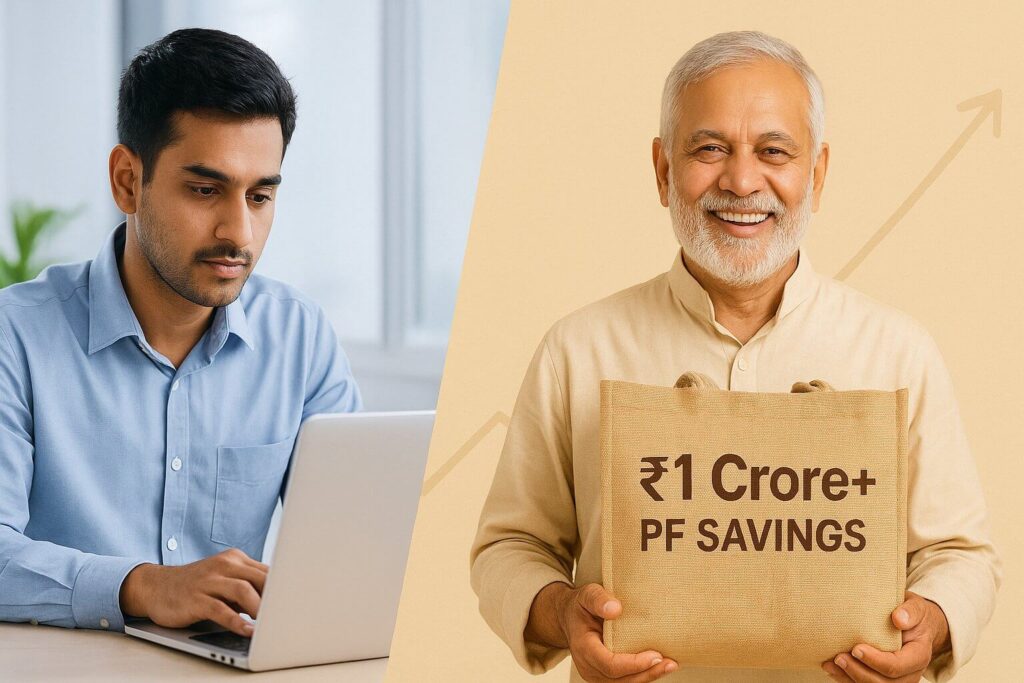

PF in India – Kyun Ignore Nahi Karna Chahiye 🏆

Socho: Tumne 23 yrs pe job shuru ki, basic salary ₹20k hai. Har month PF contribution ~₹4,800 hota hai.

35 saal tak (age 58) agar chala toh tumhara PF corpus ₹1.1 crore+ ban jayega with interest! 🚀

Aur sabse badi baat – bina tension ke, automatically.

Final Thoughts on PF in India 💬

Bohot saare youngsters PF ko bas ek salary cut samajh ke ignore kar dete hain. Lekin sach ye hai ki PF in India tumhare liye ekdum safe, tax-free aur high-return retirement savings plan hai.

👉 Short-term expenses ke liye jaldi withdraw mat karo. Long-term socho, aur apna PF future ke liye safe rakho.

Next time jab salary slip me PF deduction dikhe, sad mat feel karo. Bas bolo – “Ye mera future wealth ban raha hai boss!” 😎

📢 Iss blog ko apne doston ke saath share karo .

Together grow karte hain! 💪

Financial Planning for Young Adults in India – Avoid These Common Mistakes 🚫💰

Pehli salary ka excitement sabko hota hai, lekin agar financial planning ignore kar di toh month-end stress pakka hai. Yeh guide batayegi kaun-si common money mistakes young Indians karte hain aur unhe smartly kaise avoid karein. 💰