Buy Now Pay Later in India – Complete Guide to Benefits, Risks & Hidden Costs 💳

Soch ke dekho yaar — tum online shopping kar rahe ho Amazon, Flipkart ya Myntra pe. Ek dum mast sneakers, latest smartphone ya festive kurta set cart me add kar diya. Payment page pe jaate hi ek option aata hai — “Buy Now, Pay Later” (BNPL). Bas click karo, order place ho gaya, paise baad me do. Kya baat hai na? 😄

Aaj kal Buy Now Pay Later in India ka craze full on chal raha hai — especially hum 18–35 age group ke logon ke beech. Amazon Pay Later, Flipkart Pay Later, LazyPay, Simpl, Swiggy, Zomato — sab offer kar rahe hain. Lekin bhai, yeh sirf ek easy payment option nahi, thoda risky bhi ho sakta hai agar samajh ke use na karo.

Chalo iss blog me main tumhe BNPL ka poora gyaan deta hoon — kaise kaam karta hai, benefits kya hain, risks & hidden costs kya hain, aur kaise ise smartly use karein. (Agar tum chaaho toh RBI ke BNPL guidelines bhi dekh sakte ho: https://www.rbi.org.in/)

Buy Now Pay Later in India Kya Hai? 🛒

Simple language me, BNPL ek short-term credit service hai. Tum abhi cheez kharido, aur payment 15–30 din baad karo — kabhi-kabhi EMI me bhi split ho jaata hai.

Aur sabse badi baat — initial period me interest-free hota hai. Matlab free credit ka mazaa. Lekin bhoolna mat, yeh bhi ek type ka loan hi hai, bas physical credit card ke bina.

Kaise Kaam Karta Hai BNPL?

- Tum online/offline shopping karte ho.

- Payment method me Buy Now Pay Later select karte ho.

- BNPL provider (jaise Amazon Pay Later, LazyPay, Simpl) tumhara KYC check karke limit decide karta hai.

- Approval milte hi transaction complete.

- Due date pe payment ya EMI me repayment karna hota hai.

Example:

Rohit ne ₹10,000 ka phone Amazon Pay Later se liya. Usko 30 days ka time mila. Time pe payment kiya toh free. Late hua toh interest + late fee lag gayi.

Popular BNPL Providers in India 📲

India me BNPL kaafi options ke saath aata hai:

- Amazon Pay Later – ₹60,000 tak limit, 30 days interest-free, EMI available.

- Flipkart Pay Later – Monthly billing, selected products pe no-cost EMI.

- LazyPay – ₹1 lakh tak limit, 15–30 days repayment.

- Simpl – Bill ko 2 parts me split karta hai; Zomato, Swiggy, BigBasket pe chalega.

- Ola Money Postpaid – Ola rides, food delivery, shopping.

- ZestMoney – EMI-based BNPL for electronics, travel, etc.

Benefits of Buy Now Pay Later in India ✅

BNPL ka craze sirf marketing ka result nahi hai — sach me kuch faayde hain.

1. Instant Shopping Power

Salary aane me time hai, lekin zarurat abhi ki hai? BNPL se kaam ho jaata hai.

Example: Salary 7 din baad aayegi, lekin tumhe office bag abhi chahiye — BNPL bridge ban jaata hai.

2. Interest-Free Period

15–30 din ka free credit milta hai. Time pe repay kiya toh ek paisa extra nahi dena padta.

3. Easy Approval

Credit card ke tough approval ke bina bhi BNPL mil jaata hai. Students aur first-time credit users ke liye perfect.

4. Credit Score Improve

Time pe payment karoge toh credit history strong hoti hai — future loans ke liye helpful.

5. No Credit Card Needed

BNPL tumhe short-term credit ka benefit deta hai bina credit card ke.

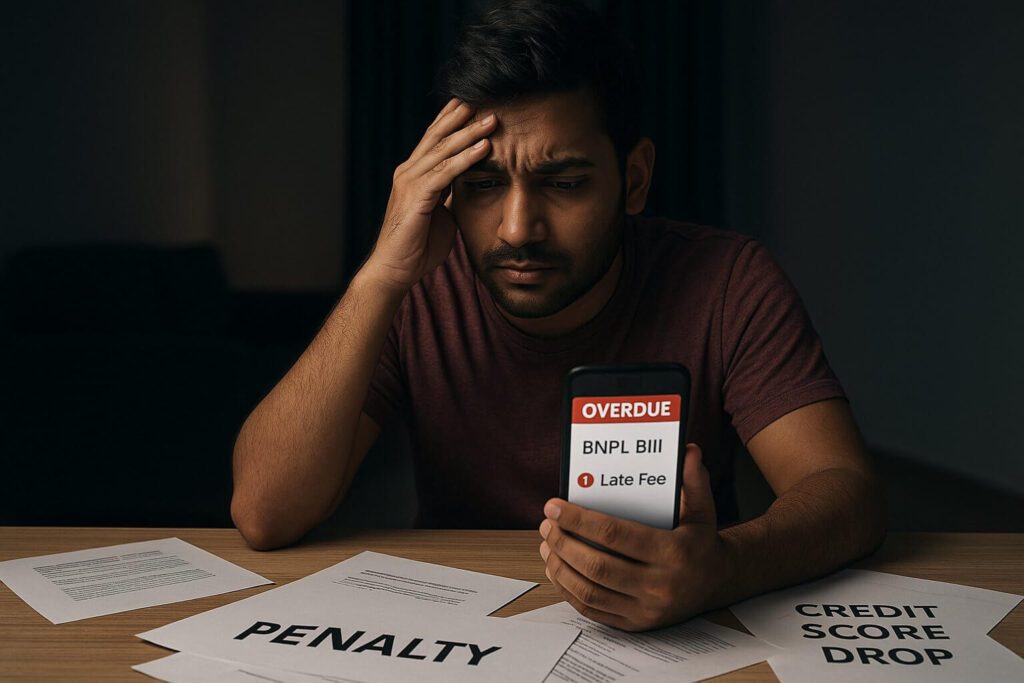

Risks of Buy Now Pay Later in India ⚠️

BNPL ka mazaa tabhi hai jab control me use karo. Varna yeh trap ban sakta hai.

1. Overspending ka Danger

Paise turant nahi dene hote, toh shopping ka mood over ho sakta hai. Month end me bill dekh ke shock lagta hai.

2. High Late Fees & Interest

Due date miss hui toh interest 24–36% yearly tak jaa sakta hai.

Example: ₹5,000 ka bill ek month late hua toh ₹300–₹500 extra charges lag sakte hain.

3. Credit Score Damage

Late payment ka direct effect CIBIL score pe padta hai.

4. Multiple Accounts ka Confusion

Agar tumne Amazon Pay Later, Flipkart Pay Later, LazyPay sab le rakha hai, toh due dates mix ho sakti hain — aur late ho sakta hai.

Hidden Costs – Jo Ad Me Nahi Batate 🕵️♂️

BNPL ke ads me “0% interest” highlight hota hai, lekin asli game T&C me chhupa hota hai:

- Late Payment Fees – ₹100–₹1,000.

- Processing Fee – EMI conversion pe ₹99–₹199.

- Bounce Charges – Auto-debit fail hua toh ₹300–₹500.

- Post-Free Period Interest – 24%+ annually.

💡 Pro Tip: BNPL lene se pehle hamesha terms read karo. “Free” ka matlab hamesha free nahi hota.

Real-Life BNPL Stories

Positive:

Ananya (Marketing Professional) ne Flipkart Pay Later se festive sale me washing machine li. ₹15,000 ka payment 20 din me clear kar diya. No interest, no late fee, credit score boost.

Negative:

Kunal (College Student) ne LazyPay use karke Swiggy orders + gaming headset le liya. Salary aane se pehle limit full. Payment late, ₹600 extra charge, credit score -50 points.

“Aapko yeh concept pasand aa raha hai toh aapko yeh wala blog bhi kaafi useful lagega  [Debt Snowball vs Debt Avalanche – Best Loan Repayment Method in India

[Debt Snowball vs Debt Avalanche – Best Loan Repayment Method in India  ]”

]”

BNPL vs Credit Card – Kaunsa Better? 🆚

Feature | BNPL | Credit Card |

Approval | Easy, low credit history needed | Good credit score required |

Interest-Free Period | 15–30 days | 20–55 days |

Rewards/Points | Rare | Common |

Credit Limit | ₹5k–₹1 lakh | Higher |

Credit Score Impact | Yes | Yes |

Fees | Hidden charges possible | Annual + late fee |

BNPL Smartly Use Karne Ke Tips 🧠

- Limit Set Karo – BNPL ko free money na samjho.

- Due Date Pe Pay Karo – Calendar reminder lagao.

- Essentials Ke Liye Use Karo – Impulse shopping avoid karo.

- Accounts Track Karo – Multiple BNPL accounts ka record rakho.

- Charges Check Karo – EMI & processing fees dekh ke hi decide karo.

BNPL ka Future India Me 🚀

Reports ke according, 2025 tak BNPL market ₹1.5 lakh crore cross karega. UPI, digital wallets, e-commerce boom ke saath adoption badh raha hai. RBI bhi regulate kar raha hai taaki customers safe rahein. (Wikipedia par BNPL ka global overview dekhna ho toh: https://en.wikipedia.org/wiki/Buy_now,_pay_later)

Lekin future me yeh tabhi benefit karega jab hum responsible repayment habits rakhenge.

Final Thoughts – BNPL Lena Chahiye Ya Nahi? 🤔

Buy Now Pay Later in India ek useful tool hai agar tum ise smartly use karo — emergencies, short-term cash gaps, ya festival shopping ke liye.

Lekin misuse — overspending, due date miss, multiple accounts — tumhara paisa aur credit score dono kharab kar sakta hai.

💬 Bottom Line: BNPL ek knife ki tarah hai — kaam ka bhi hai, khatarnaak bhi. Tumhare use pe depend karta hai.

📢 Iss blog ko apne doston ke saath share karo .

Together grow karte hain! 💪

AI in Personal Finance: 7 Tarike Jisse Artificial Intelligence Aapke Paise Ko Grow Kar Sakta Hai 💡💰

AI ab sirf robots ka magic nahi, balki aapka personal money coach ban chuka hai — jo har rupaye ko smartly grow karne me help karta hai.