Finance for Influencers in India – How to Manage Irregular Income 🎥💰

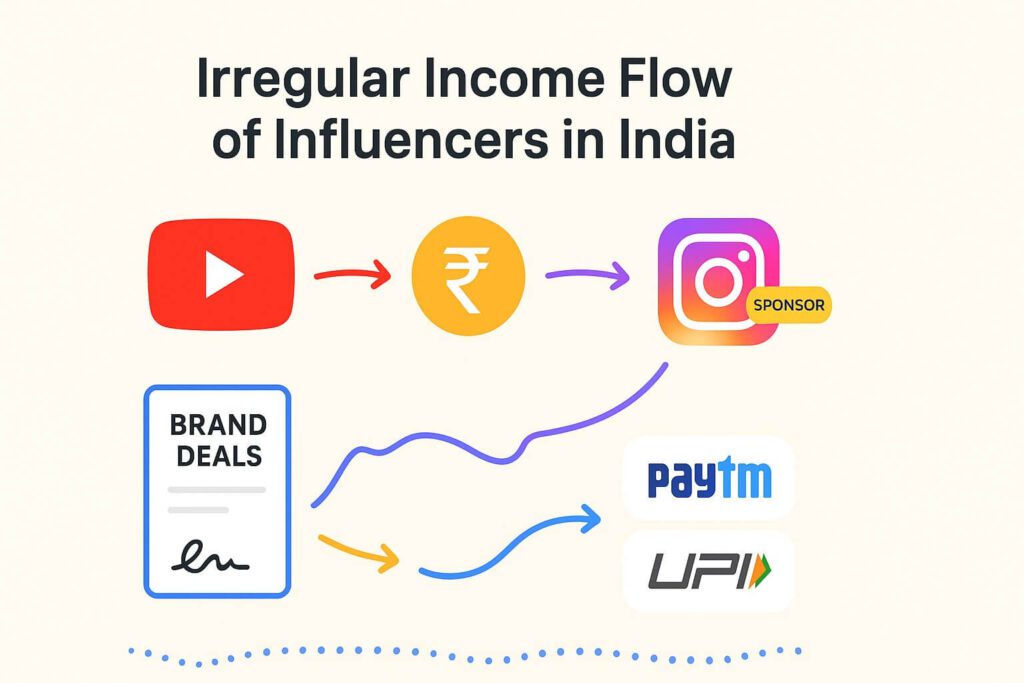

Soch ke dekho yaar – tum ek content creator ya influencer ho India me. Kabhi ek mahine me brand deal se ₹1.5 lakh mil gaya, aur agle mahine? Zero. Kabhi YouTube Adsense mast paisa de deta hai, kabhi Instagram collab ka paisa 60 din delay ho jaata hai.

Yeh hi hai influencer life ka asli scene – creative aur exciting, lekin financial side ekdum unpredictable. 9–5 job jaisi fixed monthly salary ka scene nahi hota. Agar smart finance planning nahi kiya, toh lakhon kamane ke baad bhi kuch mahino me broke feel karoge.

Is blog me hum breakdown karenge Finance for Influencers in India step by step – budgeting hacks, tax tips, savings, investments aur wo mindset jo tumhe financially stable banayega.

Kyun Zaroori Hai Irregular Income Ko Manage Karna? 🎯

Creators aur influencers ka paisa multiple jagah se aata hai:

- Brand collaborations (jo aksar late payment dete hain)

- YouTube/Instagram ads revenue (views aur season pe depend karta hai)

- Affiliate marketing (kabhi sale hota hai, kabhi nahi)

- Workshops, courses ya digital products (sales-based income)

Problem ye hai ki salaried logon ke paas ek fixed monthly salary hoti hai, but creators ko exact monthly income ka idea hi nahi hota. Result? Paisa aate hi overspending aur jab income rukti hai toh panic mode.

👉 Isiliye ek proper financial system banana must hai – taaki cash flow smooth rahe, debt avoid karo aur long-term wealth build ho.

Step 1: Khud Ko Monthly Salary Do 💵

Sabse golden rule – “Pay Yourself First.”

Apne liye do bank accounts banao:

- Business/Income Account – jitne bhi brand deals, YouTube, affiliate ka paisa aaye, sab idhar aayega.

- Personal Salary Account – jahan tum khud ko ek fixed monthly “salary” doge.

Example: 3 months me ₹3 lakh aaye toh pura udaane ke bajaye har mahine ₹50,000 apne salary account me transfer karo. Baki paisa business account me rehta hai future ke liye.

👉 Isse tumhara life ek regular job jaisa stable lagega, aur lifestyle swings avoid ho jaayenge.

Step 2: Emergency Fund = Lifeline 🛑

Influencer life = high uncertainty. Kabhi collabs ruk jaate hain, kabhi algorithm change, kabhi advertisers ka budget cut.

👉 Minimum 6–12 months ke expenses ka emergency fund banao. Agar monthly expense ₹40,000 hai → toh ₹2.5–₹5 lakh emergency fund must hai.

Ye paisa stocks/crypto me mat daalna. Best hai liquid mutual funds, FD ya high-interest savings account me.

Step 3: Budget Like a Pro 📊

Collab ka paisa aate hi shopping spree? 🤭 Ye sabse common mistake hai.

Use the 50-30-20 Rule for Creators:

- 50% Needs → Rent, food, internet, Jio recharge, travel, bills.

- 30% Wants → Zomato–Swiggy orders, Myntra shopping, Goa trip.

- 20% Savings & Investments → SIPs, mutual funds, PPF.

💡 Pro Tip: Budget hamesha apne average income pe banao, na ki peak income months pe.

Step 4: Taxes Ko Ignore Mat Karo 💸

Creators ki sabse badi galti = tax ka tension last moment pe lena.👉 Har payment me se 30% ek alag Tax Account me daalo.

Example: ₹1 lakh mila → turant ₹30,000 tax account me daal do.

Year end me ITR file karte time tumhare pas ready paisa hoga.

Aur haan:

- Agar ₹20 lakh annual turnover cross ho gaya toh GST register karna padega.

- Camera, laptop, internet bill, co-working, travel – ye sab tax deductible expenses hote hain.

(Visit Income Tax Department of India for official ITR and GST details.)

Step 5: Multiple Income Streams Banao 🌐

Sirf brand deals pe depend karna risky hai. Smart creators diversify karte hain:

- Affiliate Marketing (Amazon, Flipkart, beauty products)

- Digital Products (eBooks, templates, presets)

- Workshops/Coaching (Instagram growth masterclass, video editing)

- YouTube Ads + Memberships

- Paid Telegram/Discord communities

👉 Jitne zyada sources, utna smooth cash flow.

Step 6: Invest Like a Creator, Not a Gambler 📈

Career me tum already risk le rahe ho, finance me balance rakhna zaroori hai.

Beginner-Friendly Investments for Influencers in India:

- SIP in Mutual Funds (long-term wealth)

- Index Funds/ETFs (safe growth)

- NPS/PPF (retirement ke liye)

- Gold/Sovereign Bonds (safe hedge)

- Crypto/Stocks – max 5–10% portfolio

💡 Example: Delhi ki ek food blogger har mahine ₹2 lakh kamati hai. Usne ₹40k SIP, ₹20k NPS aur ₹60k expenses ke liye fix kiya. 5 saal me uska portfolio ₹35 lakh+ ho gaya – irregular income ke bawajood.

Step 7: Insurance = Non-Negotiable 🛡️

Ek medical emergency = saal bhar ki mehnat khatam.

- Health Insurance → ₹5–10 lakh coverage minimum

- Term Insurance → agar tum family ko support karte ho

- Gear Insurance → cameras/laptops ko cover karne ke liye (home insurance option use kar sakte ho)

“Aapko yeh concept pasand aa raha hai toh aapko yeh wala blog bhi kaafi useful lagega  [Digital Nomad Finance: Smart Money Management While Working Anywhere

[Digital Nomad Finance: Smart Money Management While Working Anywhere

]”

]”

Step 8: Retirement Planning Abhi Se 🏖️

Content career forever nahi chalega – algorithms aur trends badalte rehte hain.

👉 Har mahine thoda thoda PPF, SIP, NPS me daalo.

Goal ye rakho ki ek din tumhare assets (stocks, real estate, business) tumhe paisa banakar de, chahe tum content banana band hi kyon na kar do.

Step 9: Late Payments & Contracts Handle Karna ✍️

India me creators ka sabse bada dukh = late brand payments.

- Always sign contracts.

- 50% advance demand karo.

- 30–45 days ka timeline clearly likhwao.

- Tools like Razorpay, Zoho Books use karo invoicing ke liye.

💡 Pro Tip: Kabhi bhi ek hi agency/brand pe dependent mat raho. Multiple partners ke sath kaam karo.

Step 10: Mindset Shift – You’re a Business Owner 💼

Influencer ≠ sirf artist. Tum ek solopreneur ho.

- Income & expenses monthly track karo (Excel/Notion/QuickBooks).

- Ek CA hire karo tax planning ke liye.

- Records maintain karo brand deals ke.

- Profits ko growth me reinvest karo – better gear, ads, team.

👉 Jab tum apne content ko business ki tarah treat karoge, tabhi financial stability aayegi.

Real-Life Example: Arjun ka Journey 📖

Arjun, 26-year-old tech YouTuber, Bangalore se:

- Year 1: ₹6 lakh kamaya, sab gadgets pe uda diya, broke ho gaya.

- Year 2: ₹15 lakh kamaaya, 2 bank accounts banaye, ₹4 lakh emergency fund aur SIPs start ki.

- Year 3: ₹20–25 lakh annual income, apne aap ko ₹80k/month salary deta hai, ₹10 lakh invest kiya hua hai.

👉 Lesson: Income se zyada zaroori hai discipline aur system.

Conclusion: Mastering Finance for Influencers in India

Being an influencer India me mast hai, lekin financial side tricky hoti hai. Monthly salary wala stability nahi milta, lekin agar tum smart system banao – salary withdraw karna, budgeting, taxes ka planning, side income streams aur long-term investments – toh tum real wealth build kar sakte ho.

End of the day – content creation unpredictable hai, lekin tumhara paisa predictable hona chahiye. ❤️

🔑 Final Thought: Chahe tum YouTuber ho, Instagram creator ho ya podcaster – creativity tumhe paisa dilaati hai, lekin financial discipline tumhe wealthy banata hai. Aur wahi hai asli secret of mastering Finance for Influencers in India.

📢 Iss blog ko apne doston ke saath share karo .

Together grow karte hain! 💪

Tax Benefits for Salaried Employees in India – Complete Guide 💼💰

Salary milti hai toh khushi hoti hai, par tax cut dekh ke mood off ho jaata hai. 😅 Good news – smart planning se tum legal tarike se apna tax burden kam karke lakhon bacha sakte ho! 💼💰